Table of Contents

In February 2026, the Small Business Expo Research Desk analyzed survey responses from small business owners to better understand how rising costs are affecting margins across industries.

At first glance, the results show a divided landscape: 38.8% of businesses say their costs have increased faster than their prices over the past year, while 36.2% say they have not experienced that squeeze. Another 25.0% are unsure.

But when the data is segmented by industry, a much sharper story emerges.

Inventory pressure is heavily concentrated in product-based sectors — particularly retail, eCommerce, restaurants, and construction — while service-oriented industries are experiencing a very different cost profile.

Highlights

- 38.8% of businesses say costs have increased faster than prices

- Inventory/materials is the most cited expense among margin-compressed firms

- 81.8% of margin-compressed retail businesses cite inventory as their largest increase

- Service industries report far lower inventory exposure

- Confidence remains relatively strong despite margin pressure

The Margin Squeeze Is Real — But Not Universal

Overall, the sample is nearly evenly split between businesses experiencing margin compression and those who are not.

Among all respondents:

- 223 say costs rose faster than prices

- 208 say they did not

- 144 are unsure

This is not a uniform crisis — but it does signal meaningful pressure across a substantial portion of small businesses.

Broader national surveys have similarly noted cost pressures in goods-intensive sectors, particularly among smaller firms with limited purchasing leverage¹.

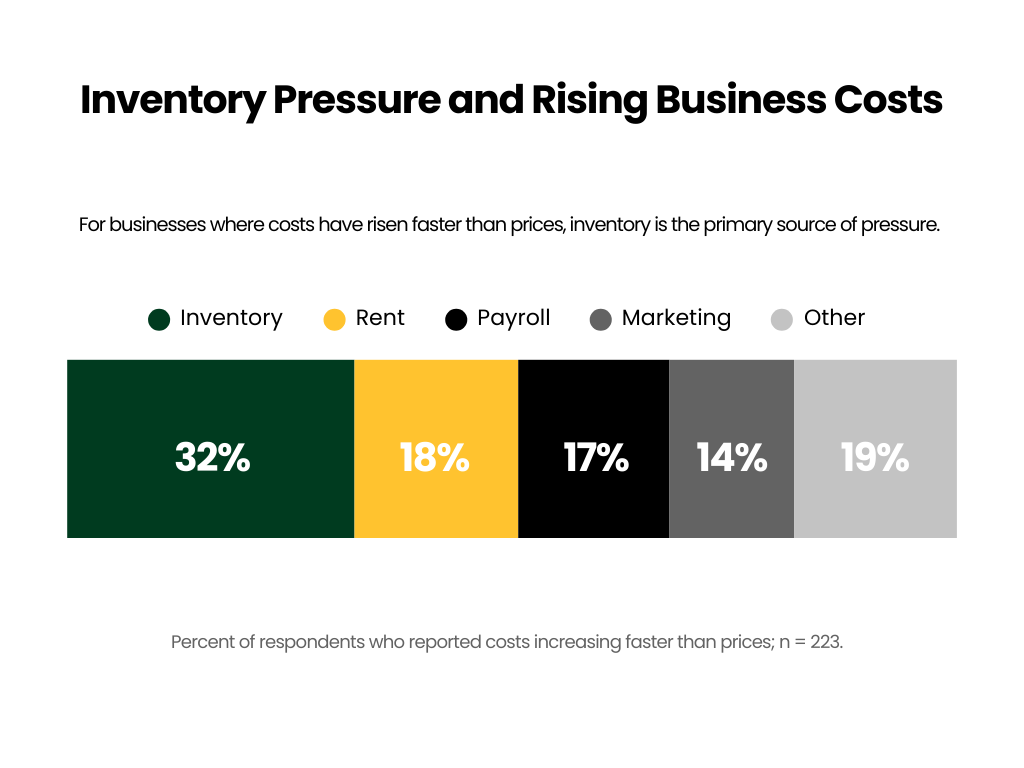

Inventory Is the Primary Pressure Point — Especially in Product Sectors

Among businesses that say costs have increased faster than prices:

- 32.3% cite inventory/materials as their largest recent expense increase

- 18.4% cite rent

- 16.6% payroll

- 13.9% marketing

Inventory stands out as the leading contributor to margin compression.

But the industry breakdown tells a clearer story.

Within Product-Based Industries:

Among businesses reporting margin compression:

- Retail/Apparel/Manufacturers/Distributors — 81.8% cite inventory

- Restaurant/Food & Beverage — 66.7%

- Construction/Engineering — 63.6%

- Consumer Products & Services — 54.5%

- eCommerce — 33.3%

In these sectors, inventory is not just one cost among many — it is often the dominant one.

Industry-level inflation exposure has varied significantly over the past two years, with product-heavy sectors facing more direct supply-chain and materials volatility than service-based industries².

Service Industries Tell a Different Cost Story

In contrast, service-heavy industries show minimal inventory exposure.

Across the full sample:

- Marketing/Advertising — 10.7% cite inventory

- Technology/IT — 10.3%

- Professional Services — 13.3%

- Legal — 14.3%

- Consulting — 12.1%

For these industries, cost pressure tends to come from:

- Payroll/labor

- Marketing investments

- Rent/space

- Software and tools

This suggests the current cost environment is not uniform — it is structurally tied to business model.

Inventory Pressure Skews Small

The revenue segmentation further sharpens the story.

Among businesses citing inventory as their largest increase:

- 85.7% are under $250,000 in annual revenue

This indicates that inventory pressure may disproportionately impact micro and very small firms, which often lack:

- Purchasing leverage

- Long-term supplier contracts

- Hedging flexibility

- Large working capital reserves

For smaller product-based businesses, inventory increases appear to translate more directly into margin compression.

Confidence Remains Surprisingly Resilient

One unexpected finding: margin compression does not appear to dramatically undermine optimism.

Among businesses reporting costs rising faster than prices:

- 49.8% are still very confident in their six-month growth outlook

- 26.5% are somewhat confident

- Only 2.7% are very concerned

Interestingly, businesses that are “not sure” whether costs outpaced prices show lower confidence levels than those who clearly report margin compression.

Clarity — even about pressure — may be more stabilizing than uncertainty.

What This Means for 2026

The data suggests the margin story in 2026 is sector-specific rather than universal.

Product-heavy industries — especially retail, restaurants, and construction — are facing disproportionate inventory-driven pressure.

Service-based industries, by contrast, appear to be navigating a different cost environment, often centered on labor and operational expenses rather than physical goods.

For small businesses, the key variable may not simply be “Are costs rising?” but:

What kind of business are you running — and which cost category dominates your model?

Final Takeaway

In 2026, cost pressures are not evenly distributed across the small business ecosystem.

Inventory inflation is heavily concentrated in product-driven industries, particularly among smaller firms, while service-based businesses face a more diversified cost profile.

Understanding where your industry sits within that split may be just as important as the size of the cost increase itself.

Footnotes

- National Federation of Independent Business. Small Business Economic Trends Report. https://www.nfib.com

- Federal Reserve. Small Business Credit Survey. https://www.fedsmallbusiness.org